The Big Head Fake?

Investors have been waiting for months, even years, to “pivot” to away from “big tech”, especially the MAG7. And perhaps with good reason. Going into the third quarter of 2024, the strong performance of cap-weighted indexes, like the S&P 500 Index, was dominated by these companies, specifically Nvidia. Like others, we agreed that this lack of market breadth didn’t seem healthy for markets in the long run. But, keep in mind, markets were adjusting to a massive generational shift – the rapid anticipated infusion of AI into business models around the globe. They often overshoot a bit both on the way up and on the way down.

Many portfolio managers, who typically rely on diversification as a risk management tool (it’s been referred to as the market’s only “free lunch”), and who were hopelessly behind their benchmarks, bemoaned this circumstance and argued it was hype equivalent to the “dot com” bubble of 1999/2000. While we generally agree with the idea of diversifying exposures, we are security-specific investors (some would say, “stock pickers”) seeking alpha at heart and would rather pass on the vast majority of stocks in an index. To our mind, risk management is about more than diversification.

Meanwhile, small cap stocks, as represented by the Russell 2000 Index (“RTY”), were languishing relative to their big cap peers on almost an historical level.

But these circumstances have been in place for some time. In short, from almost every fundamental perspective, the deck is stacked in favor of the larger, well-capitalized incumbents and we don’t see this changing, especially considering the rise of AI which requires massive capital investment for implementation. That doesn’t mean that we shun all small- and mid-size companies.

For small caps, the hurdle has been higher for portfolio entry.

That all changed in early July as markets were whipsawed by the seemingly sudden move out of big tech stocks and into small cap stocks. An apparent catalyst for the initial move appeared to be the assassination attempt in Butler, PA and the presumption of an electoral victory against a very weak opponent. Apparently, the logic revolved around:

- Lifting of a suffocating regulatory environment that increases costs for smaller companies and discourages M&A;

- Further implementation of a US-first trade policy that would create headwinds for large global companies; and

- Potentially some unwise medaling in monetary policy that would send rates lower.

In addition, there is some evidence that the unwinding of the “Yen carry trade” – essentially, borrowing in Yen at low rates and investing in higher expected return securities in Japan and abroad – had a meaningful impact. Famously, Warren Buffet had used a similar technique to go long Japanese financial institutions in 2020. As the Yen strengthened rapidly against the dollar starting in mid-July, non-Japanese traders had to liquidate securities to support more expensive principal and interest costs. There had been speculation for some time that this “cheap money” was fueling risk-taking in equity markets worldwide.

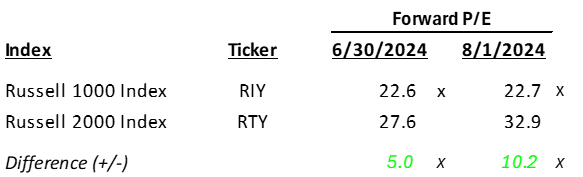

There is a narrative in the market that large cap stocks are “expensive” and small caps stocks are “cheap”.

After looking under the hood, and somewhat to our surprise, small cap stocks (as measured by the Forward P/E of the Russell 2000 Index) trade at a significantly higher multiple than large cap stocks (as measured by the Forward P/E of the Russell 1000 Index). And, the run by small caps in July has only exacerbated this reality.

We have heard the pundits, looking for a fundamental rational to justify the chase for momentum, suggest that earnings for small caps will show remarkable growth in 2025. But, while it may be true that estimates are higher today than six months ago, other than identifying the obvious macro issues to which small caps would disproportionately participate, we see little specific evidence as to why smaller companies should suddenly fundamentally outperform.

What momentum chasers might be missing is the myriad of risks that could disproportionately impact smaller companies:

- Faltering economy — Small caps as a group are more sensitive to economic downturns since many are still not self-funding, margins are thinner and there are fewer resources to weather the storm without significant interruptions to growth.

- Waning pricing power — With even the global brand heavyweights like Nike, Pepsi, P&G and Starbucks faltering in the face of a more discriminating consumer, routine COVID-era price hikes are a thing of the past.

- Higher levels of rates — Even if the Fed starts cutting in September, the absolute level of rates will remain high for some time, unless the economy gets significantly worse in a hurry (see bullet #1).

- Election uncertainty — The “Trump trade” looks like a false move two weeks hence. We expect a volatile conclusion to this election season.

It may not be too surprising to hear that we don’t like momentum-based macro trades, especially in indexes like the Russell 2000. As we are learning, the prospects and fundamentals of the constituents of an index are not homogenous. Because it is very difficult to get meaningful exposure to individual names – and requires a lot of work – most simply jump into and out of various small cap indexes as a placeholder. As we stated earlier, we like specific ideas that we can de-risk into asymmetrical opportunities.

After the Fed’s resistance to signal dovishness on Wednesday combined with Thursday’s meaningfully weaker economic data and a dead heat in the presidential race, the enthusiasm for small caps may be fading. Maybe it was just a head fake after all. And probably a good one if those who got in early take some gains soon.

Are you a Financial Professional? Then check out our new portal and get all kinds of tools and resources on multi-strategy investing, and growth.

IMPORTANT DISCLOSURES:

The Validus Rising Dividend portfolio and the Destra Multi-Alternative Fund (“the Fund”)that is sub-advised by Validus invest in Nike (NKE). The Rising Dividend portfolio invests in Microsoft (MSFT)and the Global Growth portfolio invests in Amazon (AMZN) and Meta (META). Validus has call and put options in META, MSFT, NVDA and TSLA in the Fund as part of Validus’ Hedged Alpha strategy. These stocks are all part of the MAG7.

Securities highlighted or discussed in this blog have been selected to illustrate Validus’s investment approach and/or market outlook and are not intended to represent any strategy or portfolio performance or be an indicator for how strategy or portfolio have performed or may perform in the future. Each security discussed in this blog has been selected solely for this purpose and has not been selected on the basis of performance or any performance-related criteria. The securities discussed herein do not represent an entire portfolio and, in aggregate, may only represent a small percentage of a strategy or portfolio holdings. The strategies and portfolios are actively managed, and securities discussed in this blog may or may not be held in such strategies or portfolios at any given time. These individual securities do not represent all the securities purchased, sold, or recommended and the reader should not assume that investments in the securities identified and discussed were or will be profitable. Nothing in this blog shall constitute a recommendation or endorsement to buy or sell any security or other financial instrument referenced in this letter.

Validus Growth Investors, LLC seeks to invest in companies at every stage of their growth. From startups to publicly traded companies, our research identifies inflection points that have the potential to produce meaningful growth and income for the clients we serve.

Investment Advisory Services are offered through Validus Growth Investors, LLC (“Validus”), an SEC Registered Investment Adviser. No offer is made to buy or sell any security or investment product. This is not a solicitation to invest in any security or any investment product of Validus. Validus does not provide tax or legal advice. Consult with your tax advisor or attorney regarding specific situations. Intended for educational purposes only and not intended as individualized advice or a guarantee that you will achieve a desired result. Opinions expressed are subject to change without notice. Investing involves risk, including the potential loss of principal. No investment can guarantee a profit or protect against loss in periods of declining value. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Opinions and projections are as of the date of their first inclusion herein and are subject to change without notice to the reader. As with any analysis of economic and market data, it is important to remember that past performance is no guarantee of future results.

See social media content disclosure HERE